Every blog post about the best time to trade ES futures says the same thing: trade 9:30-11:00 ET, avoid 11:30-2:00, and maybe take a look at the 2:30-4:00 close. They're not wrong. They're just useless -- because which window works for you depends entirely on what you trade.

A breakout trader and a mean reversion trader working the same 9:30-11:00 window will have completely different experiences. The breakout trader thrives on the opening volatility. The mean reversion trader gets chopped apart by the same price action. Same clock, different results.

The real answer to "when should I trade ES?" isn't a time of day. It's the overlap between when the market behaves a certain way and when your setups exploit that behavior. Here's how to figure that out.

The Three Sessions (And What Each One Actually Does)

ES futures trade nearly 24 hours, but the regular session (9:30-4:00 ET) is where the volume lives. Within those 6.5 hours, there are three distinct phases, and each one rewards a different style of trading.

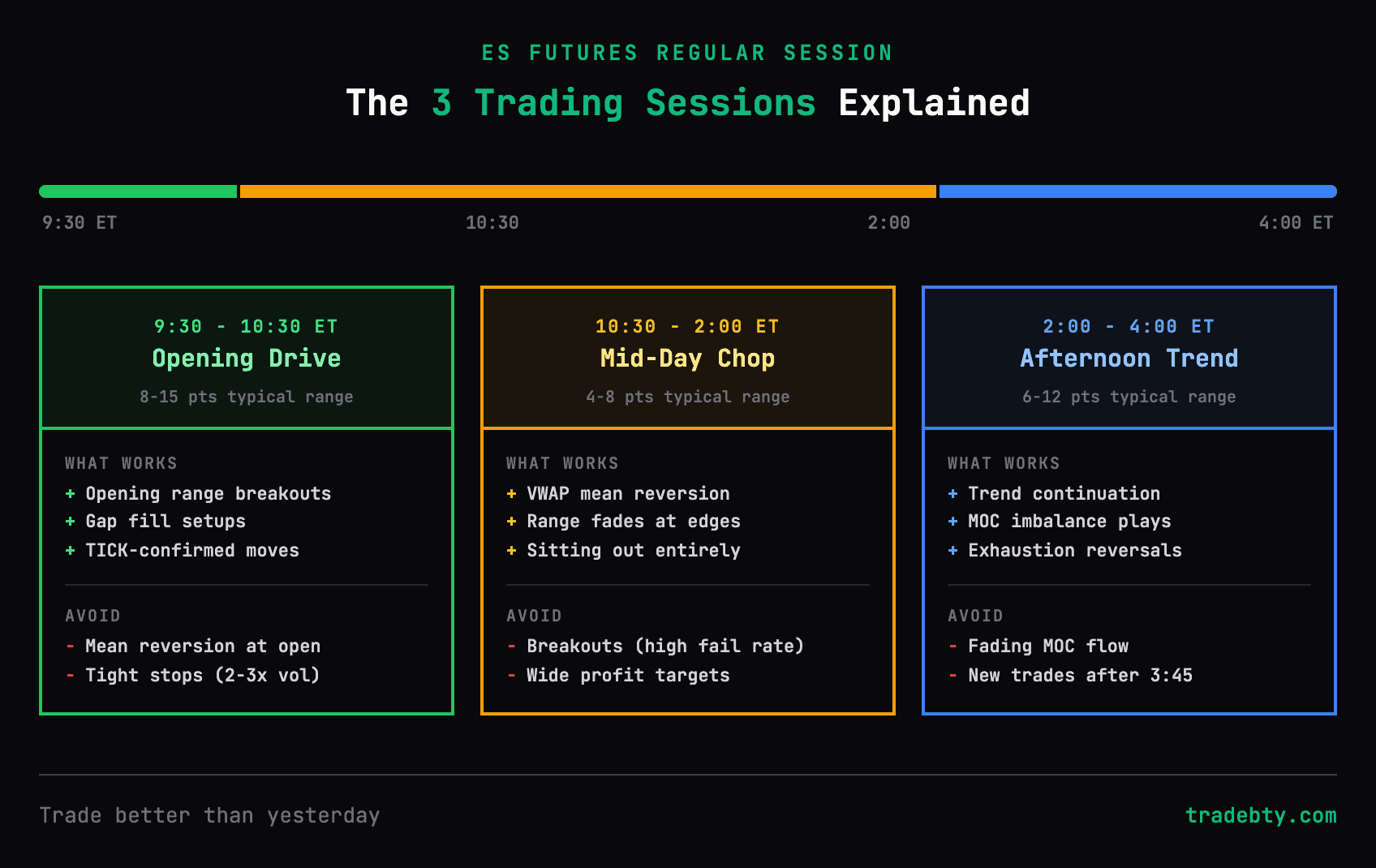

The Opening Drive: 9:30-10:30 ET

The first hour after the cash open is the most volatile, highest-volume period of the day. The opening range forms. Gaps get filled or extended. Institutional orders hit the tape. Price moves fast and often directionally.

What works here:

- -Opening range breakouts. The classic setup. ES forms a range in the first 5-15 minutes. Price breaks above or below with volume. You enter in the breakout direction, stop at the other side of the range. This is a momentum play that needs volatility to work -- and 9:30-10:00 has it.

- -Gap fills. ES gaps up 0.3% overnight. The first 30 minutes determine whether the gap fills or holds. If you trade gap fills, this is your window. After 10:30, the gap either filled or it's not going to.

- -TICK/ADD confirmation moves. When TICK (NYSE uptick/downtick breadth) is above +600 or below -600 in the first 20 minutes, it tells you whether the opening move has institutional conviction. Breakouts with extreme TICK readings are higher-probability than breakouts into a flat TICK.

What doesn't work here:

- -Mean reversion at the open. Fading the opening move in the first 15 minutes is fighting the highest-conviction flow of the day. If ES gaps up 0.5% and runs to 5860 by 9:45, shorting at 5860 because "it went too far" is a recipe for getting run over. Mean reversion works after the initial move exhausts -- usually not until 10:00 at the earliest.

- -Tight stops. Volatility in the first 30 minutes is 2-3x the mid-day average. A 2-point stop that's appropriate at noon gets clipped by noise at 9:35. If you're trading the open, widen your stops and reduce your size. On 1 ES contract, a 2-point stop is $100. A 4-point stop is $200. Use a position size calculator to make sure the wider stop still fits your risk rules.

Typical range: ES moves 8-15 points in the first hour on an average day. On FOMC days, CPI releases, or high-VIX environments, that range can double.

The Mid-Day Chop: 10:30-2:00 ET

This is the session that destroys more small accounts than any setup failure. Volume drops. Range contracts. Price oscillates in a 4-6 point band for three hours. And every choppy bar looks like the start of a breakout if you're bored enough.

What works here:

- -Mean reversion to VWAP. ES overextends 3-4 points from VWAP, then reverts. In mid-day, VWAP acts as a magnet because there's no directional conviction to push price away from it. The setup: price moves 3+ points from VWAP, exhaustion candle forms (doji, long wick), TICK confirms with a divergence. Enter toward VWAP. Stop beyond the extreme. Target: VWAP itself.

- -Range trading. If you've identified a clear range (say 5845-5852), fading the edges works when volume is low and no catalyst is pending. Buy the bottom of the range with a stop 1 point below. Sell the top with a stop 1 point above.

- -Doing nothing. This is a legitimate strategy. If your setups require momentum and directional conviction, the mid-day session offers neither. Sitting out from 11:00 to 2:00 and reviewing your morning trades is more productive than forcing three low-probability entries. The overtrading traps that blow up small accounts live in this window.

What doesn't work here:

- -Breakouts. That "breakout" above the 11:00 high? It goes 2 points and reverses. Mid-day breakouts fail at a dramatically higher rate than opening or closing breakouts because there's no volume behind them. If you're a breakout trader, this is your off-hours.

- -Wide targets. Mean reversion to VWAP works mid-day, but the move is 3-5 points, not 10. If your system needs 8-point runners to be profitable, mid-day won't give them to you. Take what the session offers or sit out.

Typical range: 4-8 points total for the entire 10:30-2:00 window. On quiet days, less than 4.

The Afternoon Trend: 2:00-4:00 ET

Volume picks up after 2:00. The MOC (Market on Close) imbalance publishes around 3:50. Institutional flows resume. If the day has been range-bound, the afternoon often picks a direction and runs. If the day has been trending, the afternoon tends to extend or exhaust the trend.

What works here:

- -Trend continuation. If ES has been grinding higher all day and the 2:00 candle breaks above the morning high, that's not mid-day noise -- it's the afternoon extension. Enter on the pullback to the breakout level. Stop below the pullback low. Target: prior day's high or the next round number.

- -MOC-driven moves. Large buy or sell imbalances at the close create predictable directional pressure in the last 30-60 minutes. $2B+ buy imbalance? ES tends to drift higher into the close. This isn't a guaranteed trade, but it's a statistical edge that works better than most price patterns.

- -Exhaustion reversals. After a full-day trend, the 3:00-3:30 window sometimes produces a reversal as profit-taking begins. If ES has run 20 points since the open and prints a lower high at 3:15 with TICK divergence, that's a potential exhaustion setup.

What doesn't work here:

- -Fading the MOC. If there's a $3B sell imbalance, buying at 3:40 because "it already dropped enough" is fighting institutional flow. MOC imbalances create directional pressure you don't want to be on the wrong side of.

- -New positions after 3:45. The last 15 minutes are for managing existing positions, not opening new ones. Spreads widen, volatility spikes, and you don't have time to manage a trade that goes against you.

Typical range: 6-12 points from 2:00 to close. Trending days can extend this significantly.

Your Setup Determines Your Session

Here's the part that generic "best time to trade" articles miss: you don't trade "the open" or "the close." You trade setups that have conditions, and those conditions align with specific sessions.

If you trade breakouts: 9:30-10:30 is your primary window. The afternoon (2:00-3:30) is your secondary. Mid-day is your off-hours -- close the platform or switch to review mode.

If you trade mean reversion: 10:30-2:00 is actually your best window, not a dead zone. VWAP reversion setups fire multiple times when price is range-bound. The open is your danger zone -- momentum overruns mean reversion entries.

If you trade trend continuation: Watch the morning for direction, but your entries are often 10:00-10:30 (after the opening range establishes direction) and 2:00-3:00 (afternoon extension). You need the first hour to show you the trend, then you join it.

If you trade gap fills: 9:30-10:00. That's it. If the gap hasn't filled by 10:30, your setup is off the table for the day.

This is why a time-based rule like "only trade 9:30-11:00" is too blunt. It works for breakout traders. It cuts mean reversion traders off from their best session. And it misses the afternoon trend entirely.

How to Find YOUR Best Trading Times

Generic advice gets you started. Your own data tells you the truth. Here's how to extract it.

Step 1: Tag Every Trade by Time Block

In your review, tag each trade as Opening (9:30-10:30), Mid-Day (10:30-2:00), or Afternoon (2:00-4:00). If you're using a spreadsheet, add a column. If you're doing voice review, just say it -- "this was a mid-day VWAP trade."

Step 2: Run the Numbers After 30 Sessions

After a month of data, calculate these separately for each time block:

- -Win rate

- -Average R:R

- -Total P&L

- -Number of trades

- -Compliance rate (playbook trades vs. improvised)

Most traders discover something specific. "My breakout trades before 10:00 win 62% of the time. The same setup after 11:00 wins 35%." That's not a market insight -- it's your personal edge mapped to the clock.

Step 3: Build Time-Based Rules

Turn the data into rules.

"IF my breakout setup triggers after 11:00 ET, THEN I skip it."

"IF I've taken 0 trades by 10:30, THEN I switch from breakout hunting to VWAP mean reversion."

"IF the market is range-bound at 2:00 and my morning P&L is positive, THEN I'm done for the day."

These rules go into your playbook. They're not restrictions -- they're filters that remove the trades your data says don't work for you.

Step 4: Review and Adjust Monthly

Your best times will shift. Summer sessions are slower -- mid-day chop extends from 10:00 to 2:30 some days. FOMC weeks compress all the action into a 30-minute window around the announcement. Quarterly expiration days have their own rhythm.

Check your time-block stats monthly. If your afternoon trades have been negative for three straight weeks, that's a signal to tighten your afternoon rules or sit out entirely until the pattern changes.

The Overnight Session: 6:00 PM - 9:30 AM ET

Most advice ignores the overnight session (also called Globex or the electronic session). For good reason -- volume is a fraction of regular hours, spreads can widen, and moves can be driven by thin liquidity rather than genuine institutional flow.

But there are two windows worth knowing:

- -European open (3:00-4:00 AM ET): London institutional flow creates a mini opening drive. If you're up early and trade mean reversion, the European open sometimes creates a VWAP reversion setup as the London and US overnight ranges interact.

- -Pre-market (8:30-9:30 AM ET): Economic releases (CPI, NFP, GDP) hit at 8:30 ET. The pre-market reaction often sets the opening range context. You don't need to trade it, but checking the 8:30-9:30 range during your morning prep tells you whether you're walking into a trending or range-bound open.

For most retail ES traders, especially those learning, the regular session is enough. Adding overnight adds complexity without adding edge unless you have a specific setup that exploits thin-liquidity conditions.

Time Filters Are Free Edge

Most traders don't track their performance by time of day. That means most traders don't know that they're profitable in the morning and negative in the afternoon, or that their mid-day trades are pure chop-induced overtrading.

The data is free. You already have the entry times in your broker statement. The analysis takes 20 minutes with a spreadsheet. And the resulting time filter -- "I don't trade between 11:00 and 2:00" -- can flip a break-even month into a profitable one by cutting your worst trades without touching your winners.

You don't need a better setup. You might just need to stop trading your existing setups at the wrong time of day. Your daily review captures the timestamp data. Your playbook holds the time-filtered rules. The gap between a losing month and a winning month might be a time filter, not a new indicator.

TBTY tracks your performance by time block automatically -- session tags, win rate by hour, and playbook compliance across the trading day. The pattern detection surfaces your best and worst windows so you can build rules around them instead of guessing. $9/mo founding rate, locked for life. Start here.

Keep Reading

- -Morning Prep Before Looking at Charts -- the 5-minute routine that sets your session plan before the open.

- -ES Futures Day Trading for Beginners -- the survival guide for going live on ES after finishing a course.

- -Overtrading a Small Account: How to Actually Stop -- mid-day chop is where most overtrading happens. Here's how to prevent it.

- -The 9-Section Trading Review Template -- the review system that captures time-of-day data for this kind of analysis.

- -Position Size Calculator -- run the math on wider stops during high-volatility sessions.

TBTY is an educational approach to structured trading review. Examples use ES futures for illustration only. Past patterns do not guarantee future results. Trading involves risk of loss. Always do your own analysis.

Want the complete framework?

This article is adapted from the TBTY framework. Get the free Quick Start Guide delivered immediately — two core ideas that fix most reviews.

Get the Free Quick Start Guide